Editor’s Note

Lithium and RREs are critical to sustaining progress in various sectors, and many developed and developing economies are pursuing policies and projects to ensure adequate access to these critical resources. For India, it is critical to ensure the availability of such resources, both by mining domestic resources and formulating enabling policies.

…………………………………………………………………………………………………………………………..

The recent discovery of Lithium in the Reasi area of Jammu and Kashmir is a significant step towards India’s green energy aspirations, especially in the case of electric car batteries. In order to diversify India’s mineral supply, the Geological Survey of India (GSI) has been conducting mapping and exploration projects across the country for various mineral commodities, including Rare Earth Elements (REE), iron ore, manganese, chromite, gold, bauxite and energy minerals like coal and lignite. On top of that, the GSI has instituted a coordinated strategy in the form of regional mineral targeting (RMT) projects to locate hidden mineral deposits.

There is, however, a need to act swiftly on the discovery and mining of vital minerals and set up investments in the downstream value chains of necessary industrial equipment, which can secure India’s green energy future and make it energy and technology independent.

Global reserves and market trends of Lithium

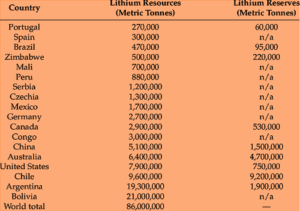

Battery-operated critical infrastructures, electric vehicles (EVs), renewable energy, and other smart gadgets are facing a bleak future due to the soaring prices and demand for Lithium-ion Batteries (LiBs). Compared to lead acid batteries, Lithium-ion batteries stand out due to their superior longevity, rapid charging, size modification flexibility, low self-discharge rate, and prolonged run duration. The major source countries of Lithium are Bolivia (21 MT), Argentina (19.3 MT), Chile (9.6 MT), called as ‘Lithium triangle’, the United States (7.9 MT), Australia (6.4 MT), China (5.1 MT) (see figure 1).

Figure: Global Resources and Reserves of Lithium

Countries have been trying harder to ensure they have enough Lithium as they do for other critical minerals. For instance, China has prioritised securing Lithium’s sources as part of its resource-intensive plan, which is reflected in its geo-economic investment projects in resource-rich countries like the Democratic Republic of the Congo, Chile, Argentina, Bolivia, and other African countries. Jiangxi Ganfeng Lithium and Tianqi Lithium are China’s two largest lithium producers. Ganfeng can produce 43,000 mt/year of lithium carbonate and 81,000 mt/year of lithium hydroxide, both suitable for battery production. In addition, Ganfeng has been increasing China’s presence in major lithium-producing nations by investing in places like Argentina’s Pozuelos and Pastos Grandes salt-lake brines. Tianqi Lithium, on the other hand, has a 51 per cent stake in the world’s largest hard rock Lithium mine in Greenbush, Western Australia, and is the second largest shareholder in the Chilean Lithium mining company Sociedad Quimica as of 2018.

India’s Lithium Deposits and Potential

Reasi Lithium resources are India’s second known lithium reserve, after a minor one discovered in Karnataka, but the first substantial deposit. It is a direct result of the increasing emphasis and efforts of the Ministry of Mines to investigate all important and critical minerals. Because lithium is an essential component of the batteries that power electric vehicles, the government is actively exploring domestic and foreign supplies. National Aluminium Company, Hindustan Copper, and the Mineral Exploration Corporation are collaborating with the GSI to create a system for studying, procuring, and mass-producing lithium-ion batteries.

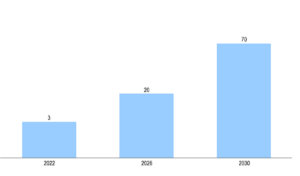

China and Hong Kong currently supply more than 70 per cent of India’s lithium requirements. Akshay Kashyap, MD of Greenfuel Energy Solutions Pvt. Ltd., said, “if India properly exploits the lithium resources in J&K, it can benefit the country’s economy, renewable energy goals, and lessen dependency on foreign suppliers”. India has set a target of tripling sales of electric vehicles by 2030, and the country’s indigenous lithium supply can help it get there. According to GSI research, the production of lithium-ion batteries in India will significantly contribute country’s effort to achieve net zero emissions by 2070.

Figure: Lithium-ion Battery Demand of India by 2030 (in GWh)

India’s Rare Earth Deposits and Potential

India’s in-situ monazite reserves were estimated at 13.07 million metric tonnes in September 2022, with 55–60 per cent of the total rare earth elements oxide found in the beach placer deposits of parts of Kerala, Tamil Nadu, Odisha, Andhra Pradesh, Maharashtra, and Gujarat, as well as in the inland placer deposits of parts of Jharkhand, West Bengal, and Tamil Nadu. India has been a major low-cost raw material supplier for the global rare earth industry. Currently, Indian Rare Earths Limited (IREL), a government-owned company, is in charge of the Indian REE ecosystem. IREL only works upstream of the rare earth industry, which involves getting monazite out of the ground and making rare earth oxides.

However, India’s midstream and downstream capabilities for rare earth, which involve processing and making finished goods, are not as well developed. It sells the oxides to companies in other countries and has to import the finished rare-earth magnets, most notably from China. The major challenge for the Indian rare earth industry has been the absence of private enterprise involvement since the government barred them from exporting beach sand minerals in 2018. IREL can process about 10,000 MT of rare earth-bearing minerals, but the production is limited by the lack of mining leases and consent clearance from the Ministry of Environment, Forestry, and Climate Change.

Step Ahead

India has had to rely heavily on imports of key minerals like cobalt, nickel, and lithium used in electric vehicles. In order to secure its supply chain, India is already engaging in resilience initiatives with countries like the US, Australia, Japan, and others to enhance its critical minerals strength all at bilateral, trilateral, and the multilateral level, for instance- 2+2 dialogues, Supply Chain Resilience Initiative (SCRI), QUAD’S Common Statement of Principles on Critical Technology Supply Chains. Nevertheless, the value chain is predicated on how many deposits are actually found and developed, but the future will depend on how organised the mineral sector will be. Thus, India’s green energy future would be best shaped with active strategies that can enhance mining exploration and reforms.

Neha Mishra

Neha Mishra is a Research Associate (Indo-Pacific Group) at the Centre for Air Power Studies (CAPS). She is doing PhD from the University of Delhi on ‘India-China Geo-economic Engagement’. Neha has an M Phil and Master’s degree in Political Science from the Department of Political Science, University of Delhi.

Her research interest focuses on India-China Geo-economic Engagement or Competition, the Role of Energy or Resource Strategy in International Politics, and China’s Resource Diplomacy. Before joining CAPS, she worked as a research intern at the Institute of Chinese Studies (ICS) and the Indian Council of World Affairs (ICWA).